The banking industry has been a pioneer and proving ground for enterprise AI. Even before other sectors experimented with pilots, financial institutions moved AI from proof of concept to production at scale. This shift has happened over the past decade, as banking’s data-rich environment, regulatory requirements, and competitive pressures pushed the industry to adopt AI before the current generative AI wave.

While traditional AI, such as supervised machine learning, is at the core of their AI initiatives, financial services organizations are increasingly adopting generative AI. S&P Global research found that about one-third of financial services companies reported using generative AI as of January 2025, compared to 21% a year earlier.

For technical executives evaluating AI strategies, banking offers critical lessons. The industry has navigated challenges that all sectors eventually face: integrating AI with legacy systems, meeting stringent compliance requirements, managing model risk, and demonstrating measurable return on investment (ROI). Understanding how banks have scaled AI provides a roadmap for any organization pursuing enterprise AI maturity.

The State of AI in Banking in 2026

AI applications in banking now span fraud detection, credit risk assessment, customer service, trading, compliance monitoring, and personalized financial advice. The technology has moved from isolated experiments to core infrastructure supporting billions of transactions.

In November 2025, Boston Consulting Group reported that retail banks could generate an estimated $370 billion in new profits annually through large-scale deployments of AI.

Banks have developed frameworks for model governance, established risk management protocols for AI systems, and created organizational structures that support AI at scale. They apply natural language processing for document analysis, and increasingly, large language models for customer interaction. This hybrid approach maximizes each technology’s strengths while managing its limitations.

3 Ways Banks Use AI in Core Operations

From the moment a customer swipes a card to the moment a loan is approved, AI is working behind the scenes to assess risk, detect fraud, and personalize the experience. The following three areas represent where that operational integration is most mature and where the business impact is most measurable.

1. Fraud detection and financial crimes

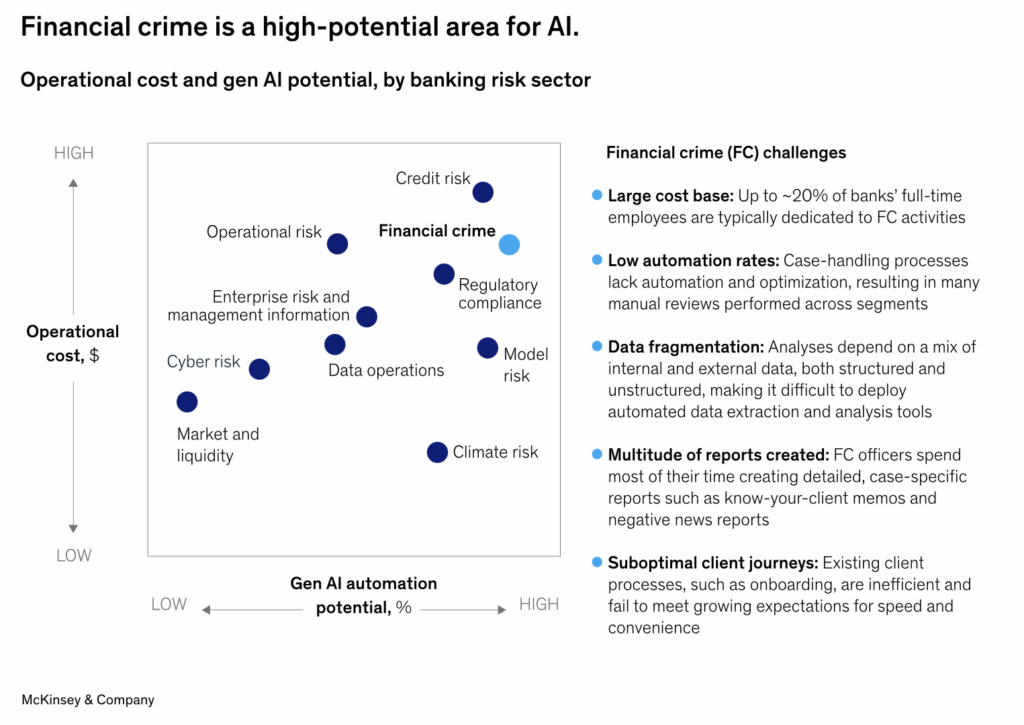

Financial crime is a high-potential area for AI because many banks still rely on people, manual processes, and fragmented data to address financial crime challenges. In addition, Deloitte reports that generative AI could enable fraud losses to reach $40 billion in the United States by 2027, while at the same time emerging as a critical tool in fraud detection.

According to McKinsey & Company research, fraud prevention consumes significant operational costs for banks, with up to 20% of their full-time employees dedicated to financial crime prevention.

Banks must detect evolving fraud patterns, identify coordinated fraud rings, and distinguish genuine customer behavior changes from account compromise. Machine learning models continuously adapt to new fraud techniques, incorporating feedback from fraud investigators to improve detection accuracy while reducing false positives that frustrate legitimate customers.

Anti-money laundering (AML) systems demonstrate similar sophistication. AI analyzes transaction networks to identify suspicious patterns that might indicate money laundering, terrorism financing, or sanctions violations. These systems process millions of transactions, flagging high-risk activities for human review while automating routine monitoring. Machine learning algorithms for money laundering detection have significantly improved detection rates while reducing the compliance burden that consumed extensive manual review resources.

2. Credit risk and lending decisions

Credit risk assessment showcases AI’s ability to improve both accuracy and fairness in banking decisions. Traditional credit scoring relied on limited variables like payment history, outstanding debt, credit utilization, and lenders’ subjective assessments, often based on the applicant’s personality, race, gender, and social status. Today, AI models incorporate hundreds of variables, including cash flow patterns, spending behaviors, and contextual economic factors, to generate more nuanced risk assessments.

This expanded analytical capacity creates opportunities for financial inclusion. AI can assess creditworthiness for customers with thin credit files by analyzing alternative data sources while maintaining rigorous fair lending standards. Banks using these approaches report both expanded customer bases and maintained or improved portfolio performance.

Commercial credit assessment, mortgage underwriting, and portfolio risk management all benefit from AI’s ability to process complex, multivariate data and identify non-obvious risk indicators. Real-time economic data integration allows dynamic risk assessment that responds to changing conditions rather than relying solely on historical patterns.

3. Customer experience and personalization

Conversational AI has transformed customer service in banking, and consumers’ expectations for personalization in banking are increasing. Mastercard research shows that Generation Z, comprising ages 14 to 29, are demanding personalization and transparency in managing their money. Gen Z is almost 2.5 times more likely than baby boomers to say they want a fast online purchase journey.

Virtual assistants handle routine inquiries, such as balance checks, transaction history, and basic account management. This automation frees human agents for complex issues requiring judgment and empathy. The technology operates 24/7, provides consistent responses, and scales instantly to handle volume spikes.

Behind these interactions, AI powers personalization engines that analyze spending patterns, life events, and financial goals to provide relevant recommendations. Rather than generic product marketing, customers receive tailored financial advice that can suggest savings strategies, identify spending anomalies, and recommend suitable financial products based on actual behavior and stated goals.

AI adapts mobile banking apps to individual usage patterns, surfacing frequently used features, predicting likely next actions, and providing contextual assistance. The result is interfaces that feel increasingly intuitive because they learn from each customer’s unique banking behaviors.

Operational AI: Behind-the-scenes Transformation

While customer-facing AI applications attract attention, some of the most significant impacts occur in back-office operations. Document processing represents a major success story. Banks process enormous volumes of documents, such as loan applications, account opening forms, compliance documentation, and trade confirmations. AI systems extract information from these documents with increasing accuracy while processing volumes that no manual team could handle.

At one Fortune-500 North American bank, capital-markets analysts were spending hours daily on manual Excel workflows with multiple files, formulas, and copy-paste steps. These manual processes created compliance risks, as their workflows could not scale with trading volumes and regulatory requirements. The team used Anaconda to build an “Excel-Python-Excel” automation framework using pandas so they could preserve their familiar Excel interfaces while automating transformation and analysis steps. They used Python scripts to create audit-ready compliance outputs. The solution was operational within three months of the team’s use of Python, and saved the company 20% in year-over-year efficiency gains.

Reconciliation and settlement processes benefit similarly. AI identifies discrepancies in transaction records, matches payments across systems, and flags exceptions requiring investigation. Work that previously required armies of analysts now happens automatically, with humans focusing on complex exceptions and process improvements.

An emerging-market bank responsible for monetary policy and oversight of dozens of commercial banks had relied entirely on manual Excel processes for financial risk analysis, taking three months to produce each stability report. Their team deployed the Anaconda platform to automate data processing and report generation to create heat maps (color-coded grids that show the severity of risk) across more than 40 economic indicators. As a result, they reduced report production time by 66%, giving analysts more time for deeper production work and giving decision makers visual tools to identify and understand systemic risks.

AI systems analyze trader communications for potential market manipulation, monitor trading patterns for insider trading indicators, and ensure transactions comply with regulatory requirements. The technology provides audit trails and explanations for compliance decisions. All of these capabilities are critical in regulated industries where systems must demonstrate how conclusions were reached.

Challenges Banks Face in Implementing AI

Despite progress, implementing AI in banking presents persistent challenges. Legacy system integration tops the list. Banks operate core systems decades old, written in languages few modern developers know, with architectures predating distributed computing. Integrating AI capabilities with these systems requires careful engineering, from APIs that bridge modern and legacy architectures to data pipelines that extract information from mainframes and deployment strategies that maintain system stability.

Model risk management creates another layer of complexity. Banks must demonstrate that AI models perform as intended, understand their limitations, and maintain them as real-world conditions change. This commitment requires robust testing frameworks, ongoing monitoring, human oversight processes, and clear protocols for model updates or retirement. Regulatory expectations continue to evolve as supervisors become more sophisticated in evaluating AI systems.

PNC Financial Services faced a challenge in updating its analytics environment. They were using proprietary platforms that were expensive, slow to develop in, and drew from a small talent pool trained in using the platform. The bank had no centralized infrastructure for data science and machine learning (ML). PNC built an “analytics competency center” based on Anaconda, and gave departments across the bank access to apply it for loss prediction, pricing, market basket analysis, scorecard models, and HR reporting. PNC included model risk management in its governance function to validate open source models within regulatory requirements. The result was a significant reduction in software costs compared to the proprietary platform they previously used.

A major European financial institution found its legacy statistical software did not provide the support needed for modern ML, with risk models requiring months to clear regulatory approval. The team was spending 60% of its time on Python package vulnerability remediation. The bank deployed Anaconda’s platform across its global data centers to give 300 risk modelers access to a governed, centralized Python environment with curated packages, reproducible Jupyter notebook workflows, and audit trails regulators could verify. The security remediation burden dropped significantly, and modelers could produce production-ready code in the same environment where they conduct their analyses.

Data quality and availability present ongoing challenges. AI performance depends on training data quality, but banking data often exists in silos, reflects historical biases, or contains gaps. Creating unified data environments while respecting privacy requirements, maintaining data lineage, and addressing historical biases requires sustained investment in data infrastructure and governance.

Talent remains a limiting factor. Banks compete with technology companies for AI expertise while requiring additional skills their competitors don’t have, such as an understanding of financial services, familiarity with regulatory requirements, ability to explain models to non-technical stakeholders and regulators. Building teams that combine these capabilities takes time and investment.

Key Lessons for Scaling AI in Banking and Beyond

The banking industry’s AI journey offers transferable insights for any organization pursuing enterprise AI maturity. Here are a few of the hard-won lessons from an industry that has been navigating the complexity of production AI longer than most other sectors:

-

Start with clear business value. Successful AI implementations in banking solve specific problems with measurable impact: reducing fraud losses, improving credit decisions, and lowering operational costs. Technology capabilities matter less than business outcomes, and early wins create the organizational support needed for sustained investment.

➔ Choose initial projects with defined success metrics, manageable complexity, and visible business impact.

-

Invest in data infrastructure first. AI quality depends on data quality. Banks that succeeded invested years building data platforms, establishing governance, and creating unified data environments before attempting sophisticated AI applications.

➔ Make improvements in data infrastructure that will minimize data silos, support quality controls, and flag historical biases.

-

Build for explainability and governance from the start. In regulated industries, black-box AI isn’t acceptable. Successful implementations include explanation capabilities, audit trails, and governance frameworks from the beginning rather than retrofitting them later.

➔ Establish a governance team to anticipate challenges and guide developers so they can anticipate and avoid approaches that will accumulate technical debt or incur regulatory risk.

-

Develop organizational capabilities alongside technology. AI success requires teams that can develop, validate, deploy, monitor, and maintain models and the applications that rely on them. Banks compete with technology companies for AI experts while also needing people who understand financial services and can explain models to regulators.

➔ Invest in talent, training, and organizational structure that provides team members with clear directives and opportunities to learn and grow professionally.

-

Plan for the long term. Organizations that succeed commit to sustained investment and treat AI systems as requiring continuous maintenance and retraining.

➔ Build institutional knowledge and create a culture of understanding among team members that prioritizes and supports steady progress over quick wins.

The banking industry’s experience with AI demonstrates that enterprise AI maturity is achievable, but it requires sustained commitment, substantial investment, and fundamental changes to how organizations operate. For technical executives willing to make these commitments, banking’s journey provides both inspiration and practical guidance.

Ready to explore what’s possible for your organization with AI? Learn more about Anaconda’s trusted tools for building AI in financial services and banking. Or contact us today to learn how Anaconda can accelerate your AI projects with its trusted distribution of open source packages.